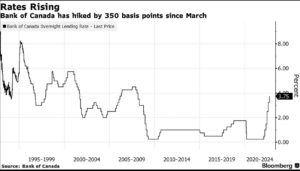

The Governing Council of the Bank of Canada raised its target for the overnight policy rate by 50 basis points today to 3.75% and signalled that the policy rate would rise further. The Bank is also continuing its policy of quantitative tightening (QT), reducing its holdings of Government of Canada bonds, which puts additional upward pressure on longer-term interest rates.

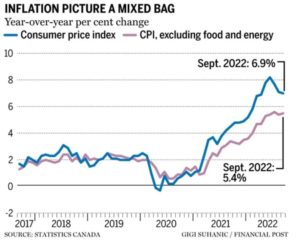

Most market analysts had expected a 75 bps hike in response to the disappointing inflation data for September. Headline inflation has slowed from 8.1% to 6.9% over the past three months, primarily due to the fall in gasoline prices. However, the Bank said that “price pressures remain broadly based, with two-thirds of CPI components increasing more than 5% over the past year. The Bank’s preferred measures of core inflation are not yet showing meaningful evidence that underlying price pressures are easing. Near-term inflation expectations remain high, increasing the risk that elevated inflation becomes entrenched.”

In his press conference, Governor Tiff Macklem said that the Bank chose to reduce today’s rate hike from 75 bps last month (and 100 bps in July) to today’s 50 bps because “there is evidence that the economy is slowing.” When asked if this is a pivot from very big rate increases, Macklem said that further rate increases are coming, but how large they will be is data-dependent. Global factors will also influence future Bank of Canada actions.

“The Bank expects CPI inflation to ease as higher interest rates help rebalance demand and supply, price pressures from global supply disruptions fade, and the past effects of higher commodity prices dissipate. CPI inflation is projected to move down to about 3% by the end of 2023 and then return to the 2% target by the end of 2024.”

The press release concluded with the following statement: “Given elevated inflation and inflation expectations, as well as ongoing demand pressures in the economy, the Governing Council expects that the policy interest rate will need to rise further. Future rate increases will be influenced by our assessments of how tighter monetary policy is working to slow demand, how supply challenges are resolving, and how inflation and inflation expectations are responding. Quantitative tightening is complementing increases in the policy rate. We are resolute in our commitment to restore price stability for Canadians and will continue to take action as required to achieve the 2% inflation target.”

Reading the tea leaves here, the fact that the Bank of Canada referred to ‘increases’ in interest rates in the plural suggests it will not be just one more hike and done.

Monetary Policy Report (MPR)

The Bank of Canada released its latest global and Canadian economies forecast in their October MPR. They have reduced their outlook across the board. Concerning the Canadian outlook, GDP growth in 2022 has been revised down by about ¼ of a percentage point to around 3¼%. It has been reduced by close to 1 percentage point in 2023 and almost ½ of a percentage point in 2024, to about 1% and 2%, respectively. These revisions leave the level of real GDP about 1½% lower by the end of 2024.

Consumer price index (CPI) inflation in 2022 and 2023 is anticipated to be lower than previously projected. The outlook for CPI inflation has been revised down by ¼ of a percentage point to just under 7% in 2022 and by ½ of a percentage point to about 4% in 2023. The outlook for inflation in 2024 is largely unchanged. The downward revisions are mainly due to lower gasoline prices and weaker demand. Easing global cost pressures, including lower-than-expected shipping costs, also contribute to reducing inflation in 2023. The weaker Canadian dollar partially offsets these cost pressures.

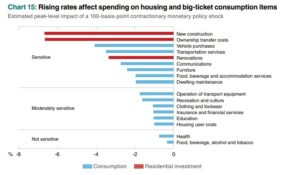

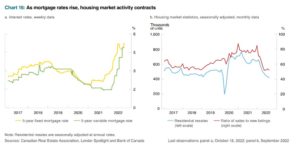

The Bank is expecting lower household spending growth. Consumer spending is expected to contract modestly in Q4 of this year and through the first half of next year. Higher interest rates weigh on household spending, with housing and big-ticket items most affected (Chart below). Decreasing house prices, financial wealth and consumer confidence also restrain household spending. Borrowing costs have risen sharply. The costs for those taking on a new mortgage are up markedly. Households renewing an existing mortgage are facing a larger increase than has been experienced during any tightening cycle over the past 30 years. For example, a homeowner who signed a five-year fixed-rate mortgage in October 2017 would now be faced with a mortgage rate of 1½ to 2 percentage points higher at renewal.

Housing activity is the most interest-sensitive component of household spending. It provides the economy’s most important transmission mechanism of monetary tightening (or easing). The rise in mortgage rates contributed to a sharp pullback in resales beginning in March. Resales have declined and are now below pre-pandemic levels (Chart below). Renovation activity has also weakened. The contraction in residential investment that began in the year’s second quarter is projected to continue through the first half of 2023, although to a lesser degree. House prices rose by just over 50% between February 2020 and February 2022 and have declined by just under 10%. They are projected by the Bank of Canada to continue to decline, particularly in those markets that saw larger increases during the pandemic.

Higher borrowing costs are affecting spending on big-ticket items. Spending on automobiles, furniture and appliances is the most sensitive to interest rates and is already showing signs of slowing. As higher interest rates work their way through the economy, disposable income growth and the demand for services will also slow. Past experience suggests that the demand for travel, hotels, restaurant meals and communications services will be impacted the most. Household spending strengthens beginning in the second half of 2023 and extends through 2024. Population growth and rising disposable incomes support demand as the impact of the tightening in financial conditions wanes. For example, new residential construction is boosted by strong immigration in markets that are already particularly tight.

Governor Macklem and his officials raised the prospect of a technical recession. “A couple of quarters with growth slightly below zero is just as likely as a couple of quarters with small positive growth” in the first half of next year, the bank said in the MPR.

Bottom Line

The Bank of Canada’s surprising decision today to hike interest rates by 50 bps, 25 bps less than expected, reflected the Bank’s significant downgrade to the economic outlook. Weaker growth is expected to dampen inflation pressures sufficiently to warrant today’s smaller move.

A 50 bps rate hike is still an aggressive move, and the implications are considerable for the housing market. The prime rate will now quickly rise to 5.95%, increasing the variable mortgage interest rate another 50 bps, which will likely take the qualifying rate to roughly 7.5%.

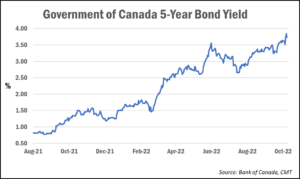

Fixed mortgage rates, tied to the 5-year government of Canada bond yield, will be less affected. The 5-year bond yield declined sharply today–down nearly 25 bps to 3.42%–with the smaller-than-expected rate hike.

Barring substantial further weakening in the economy or a big move in inflation, I expect the Bank of Canada to raise rates again in December by 25 bps and then again once or twice in 2023. The terminal overnight target rate will likely be 4.5%, and the Bank will hold firm for the rest of the year. Of course, this is data-dependent, and the level of uncertainty is elevated.

Dr. Sherry Cooper

Chief Economist, Dominion Lending Centres

drsherrycooper@dominionlending.ca